Death Of The Dollar

While the "imminent collapse" of the US dollar remains a persistent theme in contemporary financial discourse, such prognostications often occupy a disproportionate share of investment discussions relative to their historical accuracy. Headlines frequently lament the dollars demise, predict foreigners will "ditch" their reserves, or speculate a rival currency will soon seize global supremacy. However, understanding the mechanics of a reserve currency reveals why these predictions are usually more dramatic than accurate. Although, it does make for grabby headlines which I'm hoping works for this note.

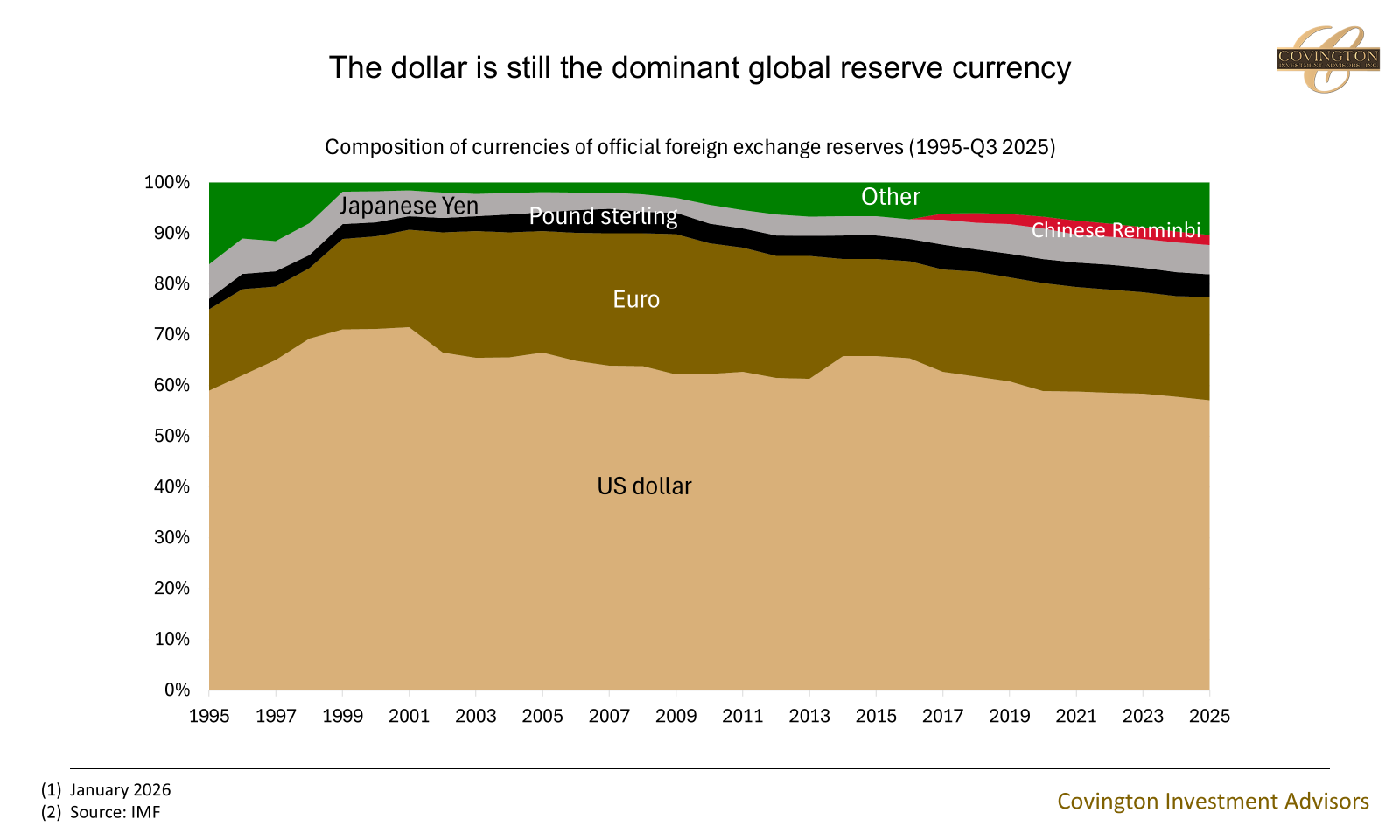

First, what is a “reserve currency”? A reserve currency is simply a foreign currency held in significant quantities by central banks and financial institutions to facilitate trade, pay off international debt, and support the stability of their own national currency. Essentially, it’s a currency that is held enough by countries like a savings account to use for transactions without destabilizing their own currencies.

Since the 1970s, the U.S. dollar has maintained its position as the world’s primary reserve currency, a status underpinned by several key economic factors. The first is overall financial market stability and efficiency. Although the US Federal Reserve is almost constantly criticized, their actions at stabilizing the economy and pace of currency expansion has largely been successful. Second, is simply the size of the US economy. The size, productivity, and growth of the US is reflected through the amount of value and thus currency that can be created and circulated to facilitate the trillions of global transactions. The third, and perhaps most important factor, is the massive trade deficit the US runs with the rest of the world. This trade deficit (buying goods and giving them dollars) is the mechanic that actually exports dollars throughout the globe. Foreigners as a whole cannot just simply “ditch” the dollar. This is due to our massive trade deficit constantly putting new dollars into the hands of foreigners. To use those dollars, they must either trade with each other or reinvest them back into U.S. assets like Treasury bonds, stocks, or real estate. A famous example of this is in the 1980s when the US was running a large trade deficit with Japan. The Japanese used those dollars to purchase large amounts of US real estate such as Pebble Beach. The bottom line is that foreigners, as a whole, cannot just simply disinvest from the dollar unless they together begin to buy more goods and services from the US than we sell to them. This would result in a US trade surplus, which we are far from.

Also in the world of foreign currencies, everything is relative. For the US to be supplanted as the global reserve currency, something would have to take its place. The euro is a hodge podge of 21 different credit markets wrapped into one currency anchored by an EU bloc with anemic growth. For the British pound there simply isn’t enough in existence to facilitate trillions in global transactions. The Chinese Yuan is built on a centrally-planned economy with capital controls specifically manipulated to ensure that they can export goods (although that is slowly changing). It’s my opinion the Chinese purposefully do not want to be the global reserve currency at this time because that would stem their entire manufacturing export model. Many of the reasons commentators use as to why a foreign currency will upend the dollar actually go against their argument when fleshed out. Other large developed economies have higher debt levels, less independent central banks, slower growth, and less functional governments.

Bitcoin and gold are the fun examples that are proposed as alternatives to the US dollar for global transactions. Bitcoin has the obvious problem of fluctuating so much in value that using it for transactions would be impractical. And if it wasn’t fluctuating in value why would speculators care about it? Ironically the value of bitcoin is usually quoted in dollars.

Gold is a topical one especially on the back of its strong price appreciation. Gold did function as the primary global reserve currency until the 1970s but fell out of favor because our economic output exceeded known gold reserves making it impractical for the growing global economic system. The most obvious drawback is that like bitcoin the supply is essentially fixed. Annual gold production increases by less than 2% per year. If the global money supply is tied to gold it cannot expand to meet the needs of a growing population, productivity, or trade. If the economy expands much quicker than the money supply, the value of money goes up, prices and wages would thus fall leading to deflation which is actually even worse than inflation. This lack of flexibility would greatly hinder modern economies. Developed central banks don’t technically “print money” (a topic for another day) - but in simple terms they can incentivize the creation of credit and thus ‘money’ by their various tools - mainly lowering interest rates or buying assets such as treasury bonds. The ability to stimulate economies during downturns and throttle credit creation during inflationary periods is a powerful tool and a large reason why modern economies are less cyclical than in the past. Milton Friedman famously illustrated that the Great Depression of the 1930s was so severe in large part because it was a deflationary shock and the Federal Reserve failed to stimulate the creation of new credit. The US money supply fell roughly 33% from 1929-1933.

However, this all doesn’t mean the dollar today won’t fluctuate in value. This is especially relevant with inflation and dollar underperformance being a key theme in recent years. Inflation affected almost every other developed currency in this timeframe - some even more so than the US. And the dollar fluctuating in value versus foreign currencies, and the dollars buying power for a basket of US goods are two different things. The US dollar index, which is a measure of the value of the United States dollar relative to six major world currencies, fell 10.7% in 2025 - it’s worst year in decades. To many this headline seems like a bad omen but in actuality it’s a purposeful policy objective of the Trump administration which views the chronic overvaluation of the dollar as a hindrance to US international trade. Stephen Miran, a key economic advisor to the Trump administration, wrote a white paper in 2024 outlining this exact position. In his own words: “The root of the economic imbalances lies in persistent dollar overvaluation that prevents the balancing of international trade, and this overvaluation is driven by inelastic demand for reserve assets. As global GDP grows, it becomes increasingly burdensome for the United States to finance the provision of reserve assets and the defense umbrella, as the manufacturing and tradeable sectors bear the brunt of the costs.” The rest of his paper can be found here.

So that’s my attempt to distill the mechanics of global reserve currencies and US dollar performance into a single email note. But more importantly, how should this all affect investment portfolios? First, investors should scrutinize claims that the dollar is going extinct or be overtaken anytime soon. The dollar's falling value did provide a boost for international investments and precious metals in 2025, but most of that is due to one time shifts related to tariff policy and a chronic valuation-gap versus US markets. Going forward I think those boosts will be less significant and US assets still have better long-term fundamentals. For precious metals in particular I think investors need to be very cautious as these are more trading instruments than long-term investments and there are signs that positioning is very crowded.

When it comes to security selection in a portfolio I don’t think it should be a guiding factor. If you were analyzing the purchase of a local private business would that investment decision be made on whether or not the dollar would remain the dominant reserve currency? Probably not. You would base that decision on the fundamentals of the business and at what price you could transact it for. It really should be no different for public securities even though they operate in a global market.

Trade policy and central bank governance is likely to remain a key source of volatility in the coming years. We saw it during liberation day in 2025, and we're seeing it now with the Supreme Court deliberation on the Trump administration’s tariffs. But predictions calling for the death of the dollar are impulsive. Ignoring the noise, focusing on the fundamentals of buying good securities at reasonable prices, and allowing them time to compound will continue to be our approach to long-term investing.