Dire Strait

Developments in the Middle East continue to unfold rapidly and have been the primary source of market volatility so far in 2026. While geopolitical crises are all unique in their own ways, they often follow similar historical patterns. Although the uncertainty surrounding the current situation remains high, I want to put the potential market effects into perspective and explain why our investment strategy is equipped to operate through them.

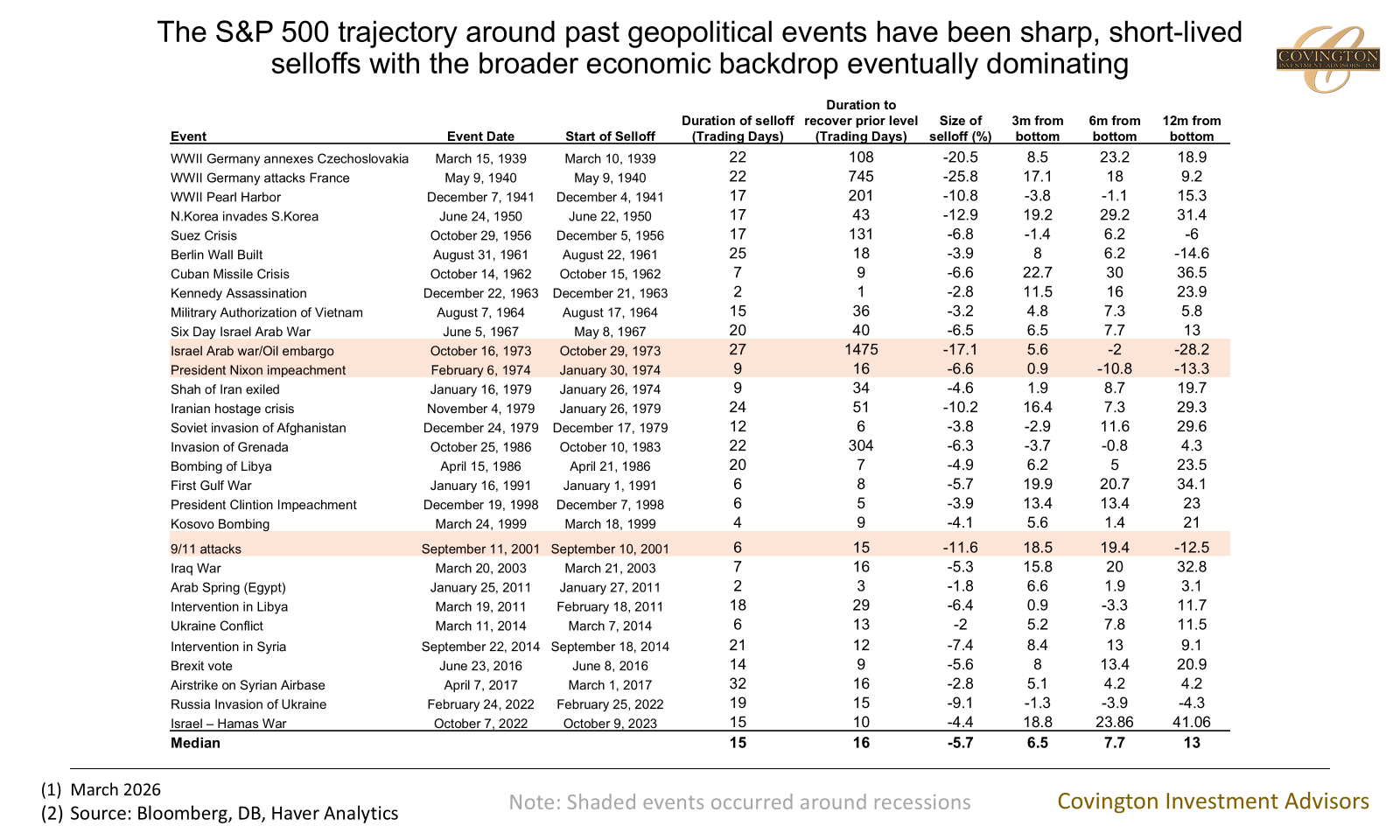

I believe it is helpful to use history as a guide to see how past geopolitical shocks affected markets in both the short and long term. Today’s chart is an update to one we sent out in 2022 at the onset of Russia’s invasion of Ukraine. History shows that geopolitical shocks tend to be short-lived with ultimately the underlying economic backdrop driving the long-term market response. The shared profile of these shocks is an initial sell-off lasting around three weeks, averaging 6–8%, followed by a recovery back to prior levels over the subsequent three weeks. Still, past performance does not guarantee future results, and we are still early in what could be a protracted period of market volatility and fundamental shifts in the global economic landscape.

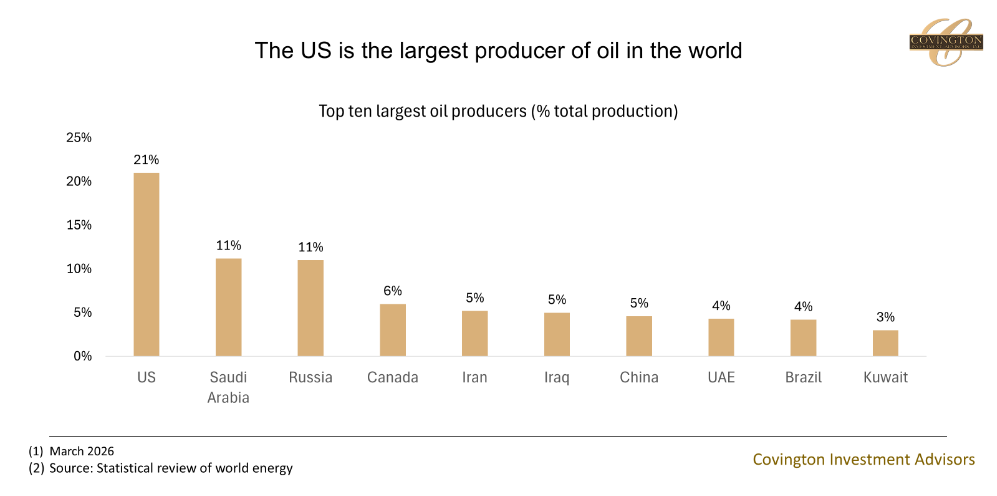

The uniqueness of this shock lies in Iran's integration into the global energy market and its influence over critical trade routes. The Strait of Hormuz is the focal point of the conflict; roughly 25% of global seaborne oil trade and 20% of global LNG pass through this waterway. Iran also has the third largest proven reserves of crude oil, behind Venezuela and Saudi Arabia. Asian economies, particularly China, are the most heavily exposed; in 2025, 11% of China’s crude oil and condensate imports came from Iran. This is especially significant in the context of the upcoming Trump-Xi statement in May.

Today, the U.S. is much more energy-independent than in the past and is more insulated than during historical episodes like the 1970s oil shocks, where prolonged disruptions spiraled enough to tip the U.S. into recession. To the extent that these events affect the domestic economy, the primary concern centers on oil prices. Energy goods and services account for less than 4% of U.S. consumer spending, about half of which is gasoline. While the U.S.’s position as a net energy exporter is enviable, oil is a global market where rising prices overseas inevitably flow through to domestic markets. Furthermore, U.S. oil reserves are mostly light oil, compared to the heavy oil passing through the Strait. While domestic refining capacity can be retooled to process different varieties, doing so requires time and capital expenditure - two variables that illustrate why the duration of the disruption is the key factor.

A sustained surge in energy costs could trigger a broader economic slowdown through wealth erosion among high-income earners facing stock market volatility, credit strain for lower-income households struggling with rising debt and fuel costs, and potential bottlenecks in AI-related investments. While current oil prices are keeping the Federal Reserve from adjusting interest rates for now, balancing these headwinds to consumer spending and upwards pressure to inflation could put the central bank in a difficult position.

Conversely, a swift conclusion to the conflict lasting less than a year would have a much more limited effect on the overall U.S. economy. It is likely the conflict will proceed in stages: the initial escalation we have already witnessed, followed by negotiations and de-escalation. However, we must be prepared for a prolonged disruption, as tensions could persist well into the future.

It is difficult to write about geopolitical events through an investment lens because developments happen so quickly. However, this environment illustrates the unique opportunities and risks of public markets, which transact long-term assets using short-term mechanics. Corporations are long-term assets whose present value is derived from future cash flows decades into the future. Yet, because their tradeable securities (stocks and bonds) can be sold daily with little friction, they are exposed to the short-term emotions of the humans transacting them. High-quality, large corporations have a track record of operating through wars, pandemics, and recessions while creating value over time. They also have a track record of fluctuating in value, often exaggerating prices on both the upside and downside.

The last decade, in particular, has illustrated the resiliency of high-quality corporations and the sharp price fluctuations that occur when short-term sentiment temporarily decouples from long-term intrinsic value. Focusing on fundamentals and treating volatility as a tactical opportunity to deploy capital has historically been a prudent approach to navigating these periods, and it continues to inform our investment perspective today.

The current conflict and the corresponding market volatility may continue for some time. However, none of the developments taking place in the Middle East change our investment approach or the financial plans we have in place for you. With our bias of investing in high-quality large cap enterprises, our portfolio compositions tend to be more defensive than the broader market. We are sticking to the fundamentals of long-term investing.

As always, we are available to discuss this further.